Once you need to activate benefits on your LTC policy, you may be subject to a waiting period, or elimination period, before benefits will kick in and begin paying. This elimination period differs from policy to policy and will be defined in your policy.

A shorter elimination period in a long-term care (LTC) policy is important because it reduces the time policyholders have to wait before their insurance benefits kick in, minimizing their out-of-pocket expenses during that period. The elimination period, also known as the waiting or deductible period, is the number of days a policyholder must receive qualified long-term care services before the insurance company begins to pay for the costs.

A shorter elimination period provides financial relief more quickly, helping policyholders manage the often high costs of long-term care without draining their personal savings. However, policies with shorter elimination periods typically come with higher premiums, as the insurance company assumes a greater share of the risk.

The typical elimination period for long-term care insurance policies ranges from 30 to 90 days, with 90 days being the most common. Some policies offer even shorter elimination periods, such as 0, 15, or 20 days, but these tend to come with significantly higher premiums. When choosing an LTC policy, it’s essential to balance the elimination period with the premium costs to find the most suitable and cost-effective coverage for your needs.

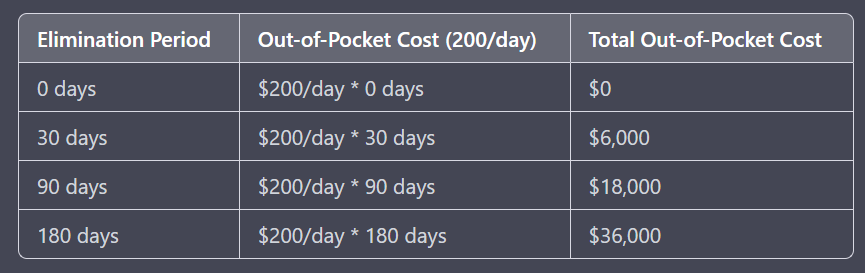

Example Costs

Here is a table showing out of pocket costs depending on how long your waiting period is:

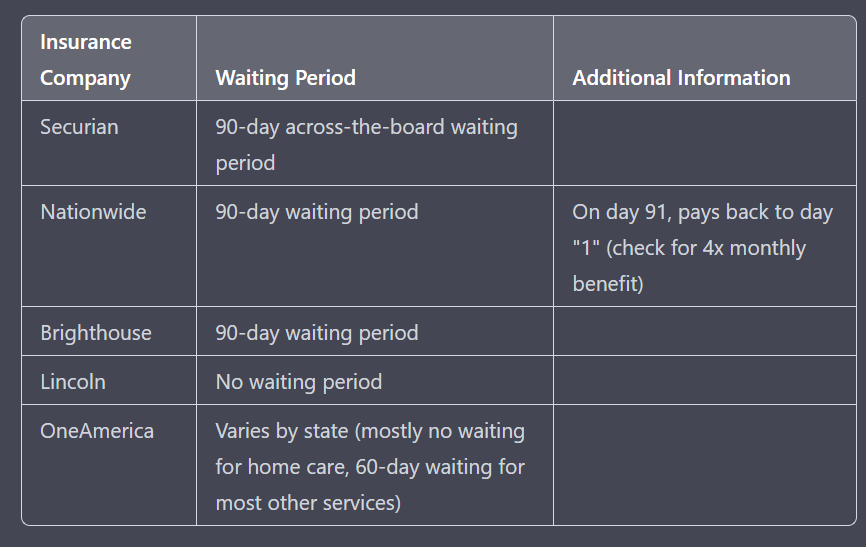

Specific Company Examples

The companies can change their offerings from time to time, but here are a few examples of what is available on the market at time of writing:

- Securian has a 90-day across-the-board waiting period.

- Nationwide has a 90-day waiting period, but on day 91 pays back to day “1” meaning if you make it to 91 days, they cut a check for four times your monthly benefit.

- Brighthouse has a 90-day waiting period.

- Lincoln has no waiting period at all.

- OneAmerica varies by state, but in most states has no waiting period for home care and a 60-day waiting period for most other services.

How Medicare Fits In The Puzzle

By the time you make a claim on your LTC policy, you’ll most likely be qualified fore Medicare’s Benefits, so we’ll discuss them here in detail.

Medicare is the U.S. government’s health insurance program primarily designed for people aged 65 and older, as well as certain younger individuals with disabilities. While Medicare primarily focuses on providing coverage for hospital stays, doctor visits, and prescription medications, it does offer some limited long-term care (LTC) benefits under specific conditions.

Under Medicare Part A, beneficiaries may receive up to 100 days of covered skilled nursing facility (SNF) care per benefit period, following a qualifying hospital stay of at least three consecutive days. The first 20 days are fully covered by Medicare, while days 21 to 100 require a daily co-payment, which may change annually. After the 100th day, Medicare provides no coverage for SNF care, and the beneficiary becomes responsible for all costs.

It’s important to note that Medicare’s 100 days of coverage are not intended for traditional long-term care needs, such as assistance with activities of daily living (ADLs). Rather, they are meant for short-term, skilled care required for recovery after an illness or injury. To qualify for this coverage, the beneficiary must need daily skilled nursing or rehabilitation services under the supervision of skilled professionals.

While Medicare’s 100 days of SNF benefits can provide some relief in terms of short-term care costs, they are not a comprehensive solution for long-term care needs. For this reason, many individuals consider purchasing long-term care insurance policies to protect themselves against the potentially high costs of extended care services, particularly in situations where Medicare coverage is insufficient or unavailable.

The Medicare Co-Payment

In 2021, the daily co-payment for days 21 to 100 of skilled nursing facility (SNF) care under Medicare Part A was $185.50 per day. This amount was required to be paid by the beneficiary for each day of care during this period, after the first 20 fully covered days. Keep in mind that these co-payment amounts may change annually.

However, you may not have to pay the co-payment out of pocket.

Some insurance plans can help cover the co-payment costs for skilled nursing facility (SNF) care under Medicare Part A. These insurance plans include:

- Medicare Supplement Insurance (Medigap): Medigap policies are supplemental insurance plans designed specifically to fill the gaps in Original Medicare coverage (Part A and Part B). Some Medigap plans cover the daily co-payment for days 21 to 100 of SNF care, easing the financial burden for beneficiaries. It’s important to note that Medigap plans are standardized, and the benefits provided depend on the specific plan letter (e.g., Plan G, Plan N) you choose.

- Medicare Advantage Plans (Part C): Medicare Advantage plans are an alternative to Original Medicare, provided by private insurance companies. These plans must offer at least the same level of coverage as Original Medicare, but they often include additional benefits, such as prescription drug coverage, dental, vision, and hearing care. Some Medicare Advantage plans may also cover the co-payment costs for SNF care, but coverage varies between plans, so it’s essential to review the plan’s details carefully.

- Long-term care insurance: Long-term care insurance policies can provide coverage for a wide range of long-term care services, including skilled nursing facility care. Some long-term care insurance policies may help cover the co-payment costs associated with SNF care under Medicare Part A. Coverage, however, depends on the specific policy and its provisions.

- Employer-sponsored retiree health plans: Some employers offer retiree health plans that may include coverage for SNF care co-payments. The extent of coverage depends on the specific plan provided by the employer.

In summary, not all plans are created the same, and thinking through how you might pay for care during the elimination period on your policy, if any, is important. Most who buy hybrid long-term care insurance plans are higher net worth and cutting a check for $200-$300/day would be possible if only for a limited period of time.

Summary of Market Offerings

Here is a table showing what is available from a few of the major carriers.

If you’d like a personalized comparison quote of these companies, and more, complete a free quote request online.

Table of Contents

Free, Personalized Side-by-Side Quotes from Our Honor Roll insurance companies, all A+ and A++ rated.