Lincoln MoneyGuard Fixed Advantage

Lincoln MoneyGuard Fixed Advantage is the latest product from Lincoln Financial Group. Many Financial Advisors recommend this plan to their clients, but is it the best bet for you in March of 2026? We’ll talk about the pros and cons.

This policy is known for its unique features and solid coverage, but in 2026 it is well worth shopping the competition as well. Given that, we’ll also look at several A+ competitors and how they stack up.

Lincoln essentially pioneered this type of Hybrid policy. They built a huge network of independent agents and banks and even Financial Advisors to sell their policies. Because of this, many times we see clients who’ve received a Lincoln quote but have not compared to others. Often, they’re shocked at how much more in benefits dollars they can get from other companies.

Key Features

- Combination of Life Insurance and Long-Term Care Coverage: Lincoln MoneyGuard Fixed Advantage combines life insurance and long-term care coverage, guaranteeing your premium cost is put to use either through long-term care benefits or as a death benefit for your beneficiaries.

- Flexible Premium Payment Options: Lincoln MoneyGuard Fixed Advantage offers various premium payment options, including:

- Single-pay

- 5-pay

- 10-pay.

This flexibility enables you to choose a payment schedule that aligns with your financial situation and goals.

Residual Death Benefit: This hybrid policy provides a guaranteed death benefit, ensuring that if long-term care is never needed, your beneficiaries will receive a payout, protecting your financial legacy and offering peace of mind to your loved ones. But even IF long-term care is needed, the Residual Death Benefit feature will provide a payment to your beneficiary even if benefits have been exhausted as defined in your policy.

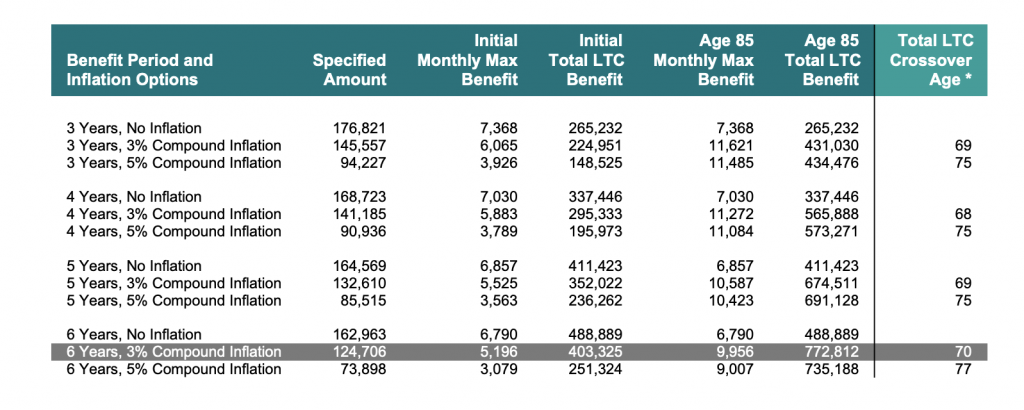

In the example we looked at, a $125,000 premium generated a death benefit of $124,706 and a Residual of $6,235.

Nationwide, on the other hand, offered $24,150 in Guaranteed minimum death benefit! That’s a big difference.

Return of Premium: Lincoln MoneyGuard Fixed Advantage includes a return of premium feature, allowing you to surrender the policy and receive a portion of your premiums back should your financial goals change in the future. The amount you receive depends on how long you’ve held the policy, but often is static.

For a 63 year-old Female in Virginia with a “Couples Discount” underwriting class, the Surrender Value was 70% of premium paid with Lincoln and 92.8% with Nationwide, while Securian built up Surrender value over time to exceed 100%!

Ready to explore Lincoln MoneyGuard Fixed Advantage in more detail? Compare it to other hybrid long-term care insurance policies with a personalized side-by-side quote from LTC Tree.

Zero- Day Elimination Period: Unlike other hybrid long term care insurance policies, Lincoln MoneyGuard Fixed Advantage has a 0 day elimination period. This means you start receiving your LTC benefits once you go on claim. This is a nice feature, but Nationwide has a similar feature (though the mechanics are different).

Inflation Protection: To ensure your policy’s benefits keep pace with the rising cost of long-term care, Lincoln MoneyGuard Fixed Advantage offers optional inflation protection riders to maintain the value of your policy benefits over time.Options include No Inflation, 3% Compound Inflation, and 5% Compound Inflation. Check out our Inflation Protection guide for complete details on what may be best for you.

Guaranteed Benefits: LTC Benefits are guaranteed as long as all scheduled premiums are paid on time and in full and you have not taken out any loans, withdrawals or surrenders for the life of the policy.

50% Cash Indemnity

While Brighthouse, Nationwide, and Securian offer 100% of LTC benefits as cash, Lincoln offers 50% of benefits as “Flex Care Cash” Access cash to compensate caregivers, including spouses or family members.

Offering 50% of benefits as “Flex Care Cash” for compensating caregivers is useful for:

- Personalized care: Families can choose care arrangements tailored to their needs and preferences, providing the most appropriate care for the recipient.

- Reduced burden: Compensating family caregivers helps alleviate financial strain and emotional stress, enabling better work-life balance.

- Familiar environment: Care recipients can receive care in their own home, improving emotional well-being and overall quality of life.

- Flexibility: “Flex Care Cash” allows families to allocate resources according to their unique needs and adapt to changing circumstances.

Important Riders

With Lincoln’s policy, you have a few decisions to make regarding riders. One is the duration of Long-Term Care benefits, with options ranging from 3 to 6 years. In our analysis, the 6-year benefit period paired with a 3% Compound Inflation rider nets the most age 85 LTC benefit while balancing Life Insurance benefits should no LTC be needed.

Discounts

Lincoln offers a discount of about 9% for policyholders who are married or have a partner. There is no requirement that your spouse apply or purchase coverage, the discount applies regardless.

There are generally no other discounts for hybrid LTC policies, and this is typical across all companies.

Sample Policy Designs

Here are different benefits available to our sample 63 year-old Female with a “Couples Discount” paying a single premium of $125,000:

If reading this table looks like Greek, you’re not alone! Get your personalized comparison quote and we’ll provide a personalized quote AND explanation of what may be best for your particular scenario. As independent agents, we are able to quote multiple carriers and find out what optimizes your premium dollars.

How Lincoln Compares

Lincoln essentially invented this type of policy, but other very highly-rated insurance companies have jumped in to compete, very strongly, for your premium dollars.

Securian

As of March of 2023, Securian’s SecureCare III ranks above Lincoln for nearly every case we look at when maximizing for Long-Term Care benefits. Securian has a 90-day elimination period, versus a 0-day waiting period with Lincoln. Securian offers a superior full cash indemnity vs the 50% Lincoln offers. You can request a quote here to see how ALL companies stack up, if curious.

Nationwide

When considering the same premium outlay, Nationwide’s Care Matters II also ranks above Lincoln benefit-wise. Nationwide generally has a higher Guaranteed Death benefit, higher monthly and total LTC benefits, and pays 100% of LTC benefits in cash. They pay back LTC coverage to day 1 assuming you need care for at least 90 days, making their policy closest to Lincoln’s in that regard.

Brighthouse

Once again, when configured appropriately, Brighthouse SmartCare will offer you more age 85 LTC benefits, higher death benefit, and a higher surrender value in most cases. Brighthouse is, by far, our go to option in New York but competes well in other states.

Brighthouse offers an indexed Inflation Protection, but we typically recommend their 5% Fixed inflation in most designs. Your age and health will factor in to whether Brighthouse is better than the others.

OneAmerica

This option is more of a toss-up, but worth investigating. OneAmerica AssetCare can be quite similar to Lincoln in some ways, because it is a reimbursement benefit (not cash indemnity). For couples, AssetCare is going to be superior in some ways, with a few interesting quirks and caveats such as a second-to-die Life insurance benefit. A joint bucket of LTC benefits is nice, with an Unlimited benefits option as well.

Compare For Yourself

We’ve developed a proprietary quoting tool that will generate side-by-side comparisons customized to your age, state, health, and will maximize discounts based on marital status and good health. Request a quote from us today to get this comparison at no charge.

Lincoln MoneyGuard Fixed Advantage offers a progressive approach to hybrid long-term care insurance, with features designed to address your evolving care needs.

Eager to make an informed decision? Request a side-by-side quote comparison from LTC Tree to find the best hybrid long-term care insurance policy prepared just for you!

Historical MoneyGuard Policies

The current “Fixed Advantage” policy series rolled out in 2022 and was preceded by:

- MoneyGuard (2011)

- MoneyGuard II (2014)

- MoneyGuard III (2019)

A re-price in early 2023 made the policy more competitive, but in our comparisons it often still lags behind others.

Financial Ratings

Lincoln’s financials rank well above average, and as of November 9, 2022, their illustration reported the following rankings:

- AM Best: A (3rd highest of 16)

- Standard and Poor’s: A+ (5th highest of 19)

- Moody’s: A1 (5th highest of 19)

- Fitch A+ (5th highest of 19)

What even is a Financial Strength rating? Well, it’s an assessment of an insurers ability to meet its financial obligations. Before buying insurance, check insurers’ financial strength ratings for stability and reliability. While important, don’t solely rely on these ratings; also consider customer service, claims handling, and suitable coverage options.

Lincoln introduced their first MoneyGuard product in 2011. It was groundbreaking in that it allowed consumers the option to pay a single premium and get two benefits: Life Insurance and Long Term Care.

Before the hybrid policy, most consumers bought “traditional” policies which had no life insurance benefit if unused, and lifetime payments due each and every year.

More than a few of these pay as you go LTC insurance plans have experienced rate increases as well.

By paying upfront, or over 10 years, you can eliminate ANY risk of rate increases with a hybrid policy.

Table of Contents

Free, Personalized Side-by-Side Quotes from Our Honor Roll insurance companies, all A+ and A++ rated.